Asian equities tumbled on Wednesday as traders grappled with the surprise political storm in South Korea, where martial law was imposed and lifted only hours later. At the same time, a no-confidence vote in France put the euro in the spotlight.

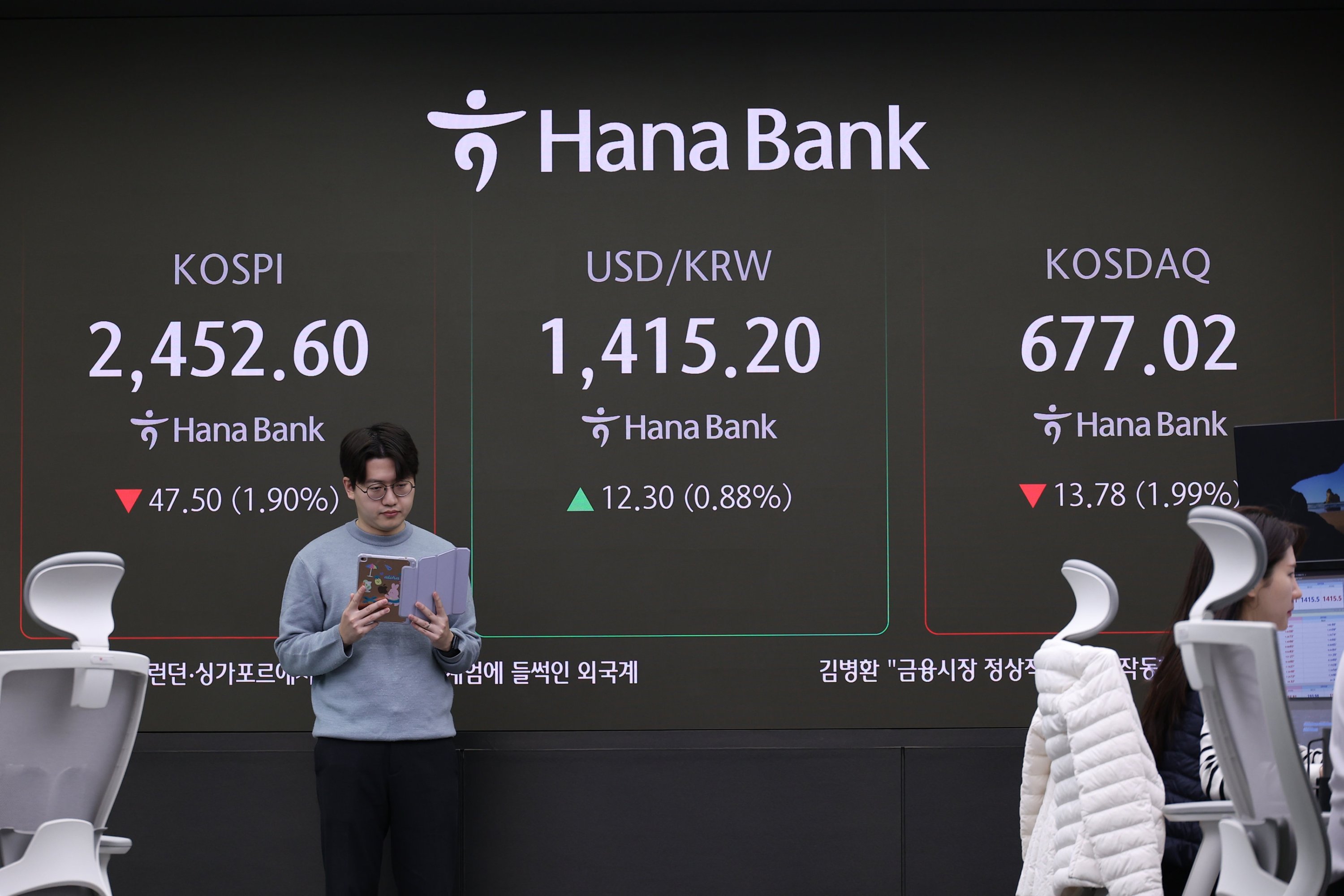

South Korea's won, buoyed by suspected intervention, was stable but remained close to the two-year low against the dollar that it hit late on Tuesday. The benchmark KOSPI index was down 1.3%, taking its year-to-date losses to more than 7% and making it the worst-performing major stock market in Asia this year.

That left the MSCI's broadest index of Asia-Pacific shares outside Japan, which counts Samsung Electronics as one of its top constituents, mainly flat as most Asian markets aside from South Korea rose.

South Korean President Yoon Suk Yeol said on Wednesday he would lift a surprise martial law declaration he had imposed just hours before, backing down in a standoff with parliament which roundly rejected his attempt to ban political activity.

"Martial law itself has been lifted but this incident creates more uncertainty in the political landscape and the economy," ING senior economist Min Joo Kang said.

"We are concerned that these events could impact South Korea's sovereign credit rating, although this is uncertain at this stage. However, this is a scenario that could happen."

South Korea's finance ministry said it was prepared to deploy unlimited liquidity into financial markets if needed, with the Yonhap news agency saying the financial regulator was ready to deploy 10 trillion won ($7.07 billion) in a stock market stabilization fund.

"A bit of uncertainty here given how the events played ... that can fuel some rush to safety. But Korean authorities appear to be moving quickly to stabilize markets, and the impact is likely to be short-lived," Saxo's chief investment strategist Charu Chanana said.

Still, the jolt to the market from East Asia stoked further worries of uncertainties around the globe, with investors already reeling from political turmoil in France that has weighed on the euro, which stood at $1.051675.

The single currency is down 4% since the start of November when investors started bracing for widely expected tariff-heavy policies from the incoming Trump administration.

French bond futures fell 0.11% while European stock futures were little changed ahead of French lawmakers' vote on Wednesday on no-confidence motions, which are all but certain to oust the fragile coalition of Prime Minister Michel Barnier.

"If the government collapses, emergency legislation will likely be adopted to avoid a government shutdown ... the spread between French and German 10-year government bond yields can further move against the euro," said Carol Kong, currency strategist at Commonwealth Bank of Australia.

On the macro side, investors are hoping for more cues to gauge the policy path the Federal Reserve (Fed) will likely take next year, with a much-anticipated November employment report due on Friday.

U.S. job openings increased solidly in October while layoffs dropped by the most in 1 to 1/2 years, data showed on Tuesday, suggesting the labor market continued to slow in an orderly fashion even as another survey showed employers were hesitant to hire more workers.

Markets are now ascribing a 72% chance of a 25 basis point cut this month, with 80 bps of cuts expected by the end of next year.

U.S. central bankers said they continue to believe inflation is heading down to their 2% target and signaled support for further rate cuts ahead, but none pushed strongly for or against doing so when they next meet to set rates in two weeks.

The spotlight now turns to Fed Chair Jerome Powell, who will give on Wednesday what are expected to be his last public remarks ahead of the meeting.

The dollar index, which measures the U.S. currency against six rivals, was at 106.3. The Australian dollar fell to four-month lows as surprisingly soft economic data led markets to bring forward the likely timing of future rate cuts. The Aussie was last down 0.7% at $0.6442.

Oil prices inched higher after gaining more than 2% in the previous session as Israel threatened to attack the Lebanese state if a truce with Hezbollah collapses, and as investors positioned for OPEC+ to announce an extension of supply cuts this week.